Are 50 Year Mortgages Available? (What’s Real, What’s Rumor, and What Borrowers Should Do)

By Fabion Medhanie · March 12, 2026 · 9 min read

If you’ve been scrolling the news or watching mortgage clips, you’ve likely seen the question: are 50 year mortgages available? I get why it’s everywhere—prices are high and rates have hovered above 6%, so a longer term can sound like relief. Let’s cut through the noise and cover the facts, the risks, and the practical moves you can make now.

Short answer: No, 50‑year mortgages aren’t available from qualified lenders today

Bottom line: No, 50-year mortgages are not currently available in the U.S. from qualified mortgage lenders. Right now, the 50‑year mortgage is mostly a policy idea being floated by some policymakers—not a product you can apply for with a standard lender.

Key point: There’s no implementation timeline, no qualification standards, and no approved policy. If you’re asking, “Can I apply for a 50‑year mortgage today?” the short answer remains no.

Why the idea is getting attention

People are talking about 50‑year mortgages because affordability is tight. When home prices are high and rates stay above 6%, monthly payments climb fast—often pushing buyers past their comfort zone and lender limits like debt‑to‑income (DTI).

The concept is simple: spread the same loan amount over more payments.

- A 30‑year mortgage has 360 payments.

- A 50‑year mortgage would have 600 payments.

More payments generally mean a lower monthly bill. That’s the draw.

What actually happened recently

The idea grabbed major headlines in November 2025:

- On November 9, 2025, President Trump proposed 50‑year mortgages.

- Reports said FHFA Director Bill Pulte called it a “complete game changer” for affordability.

Important: headlines aside, there is still no official rollout plan—no published “how to qualify,” no rate guidance, and no agency rule changes yet.

Why 30 years is the common cap today (the big roadblock)

Most headlines skip this: the U.S. mortgage system has structural guardrails that make a simple shift to 50 years difficult.

Qualified Mortgages (QM) are capped at 30 years

Most conventional loans are Qualified Mortgages (QM), built around federal rules that reduce risk for borrowers and lenders. A core rule: QMs cap terms at 30 years under standards tied to the Dodd‑Frank Act’s Ability‑to‑Repay (ATR) requirements.

Fannie Mae and Freddie Mac typically limit terms to 30 years

Most mortgages are sold to Fannie Mae and Freddie Mac, and both limit terms to 30 years. Loans over 30 years are usually non‑conforming and ineligible for purchase by those agencies.

Key point: A lender could technically write a longer loan, but if it can’t be sold into the usual pipeline, it becomes more expensive and harder to manage—so the market rarely offers it.

Reality check: Even if a longer term is “possible,” it’s not automatically practical in the current mortgage system.

The closest options today: 40‑year terms and rare exceptions

If you’ve heard about loans longer than 30 years, you’re likely hearing about limited cases like 40‑year terms. Those exist—but they’re rare and nonstandard.

- Some 40‑year nonqualified mortgages exist for purchases in limited cases.

- Longer terms can also appear in loan modifications for borrowers in hardship.

These are not widely offered conventional products.

Would a 50‑year mortgage really help? The pros and cons

I’ll be direct: longer terms lower monthly payments but usually increase long‑term cost and risk. Walk through the tradeoffs before you get emotionally attached to a “lower payment.”

Potential pro — lower monthly payments

The main benefit is a lower monthly payment. That can help some buyers qualify under DTI targets like 43%. For example, one public scenario shows only a small monthly reduction when stretching the term to 50 years.

Important: Even a slightly lower payment can be the difference between approval and denial for some borrowers.

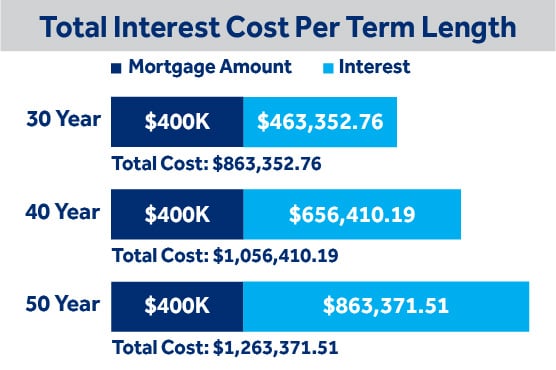

Major con — much higher total interest

The real cost shows up in total interest paid over the life of the loan. Here’s a hypothetical comparison many analysts use to illustrate the tradeoff:

| Aspect | 15‑Year Loan | 30‑Year Loan | 50‑Year Loan (Hypothetical) |

|---|---|---|---|

| Interest Rate | 5.49% | 6.24% | 6.99% |

| Monthly Payment (on $400k) | $3,266 | $2,460 | $2,404 |

| Total Interest | $187,918 | $485,695 | $1,042,216 |

| Total Loan Cost | $587,918 | $885,695 | $1,442,216 |

In this example, the monthly difference between 30 and 50 years is only $56, yet the total interest jumps dramatically. That’s the danger critics point to—a small monthly gain for a huge lifetime cost.

Likely con — higher rates and stricter rules

If longer terms ever became widely available, many expect lenders to charge higher rates (often discussed as a 0.5%+ premium) and apply stricter underwriting to manage long‑term risk. The longer the horizon, the more unknowns: job changes, illness, market cycles, and life events.

UBS and other analyses — payment relief may be marginal

Several major analyses suggest the monthly relief may be smaller than headlines imply once higher pricing is factored in. The result could be a minor payment drop but far greater total cost.

Expert guidance — use caution

Many experts advise caution. Longer terms can amplify financial risk and feel like relief now while locking you into decades of higher interest.

What lenders are saying (an example from Florida)

This isn’t just a Washington or Wall Street debate. Local lenders are clear: 50‑year mortgages are not on the product menu today. For example, Florida lenders like MIDFLORIDA have confirmed there’s no 50‑year product available.

Why this trend matters even if the product doesn’t exist

The conversation highlights where borrowers are hurting: payments feel out of reach, inventory is tight, and people are looking for anything that lowers the monthly number. As a veteran and loan officer, I keep it simple: a lower payment helps only if it doesn’t create bigger long‑term harm.

If you’re stressed about payments — realistic options to ask about now

Since “are 50 year mortgages available” is basically a no today, here are practical, real‑market moves to explore. They aren’t magic, but they’re achievable.

1) Consider a smaller loan amount (even temporarily)

Reducing the loan size is often the most direct way to hit a payment target: choose a lower price point, save for a bigger down payment, or ask for seller credits to reduce upfront costs. Buying slightly less house is often the most reliable way to protect your budget.

2) Use the 30‑year fixed and plan to refinance

The 30‑year fixed is the standard for a reason: wide availability and predictable guidelines. If rates fall later, refinancing can lower your payment without adding decades of interest. No one can promise future rates, but this is a common, practical path.

3) Ask about temporary rate buydowns

Temporary buydowns reduce the rate for the first year or two and can ease early payments while you stabilize. Not every seller or lender will offer them, but they’re worth discussing.

4) If you’re in hardship, ask about modification options

Longer terms like 40 years sometimes appear in loan modifications for homeowners in financial distress. That’s a keep‑your‑home option for tough seasons, not a routine purchase strategy.

FAQs — fast, clear answers

Are 50‑year mortgages available in the U.S. right now?

No. They are not available from qualified mortgage lenders.

Are they legal?

The idea itself isn’t “illegal,” but the mainstream system is built around Qualified Mortgage rules and 30‑year caps, plus Fannie/Freddie term limits.

Why can’t lenders just offer them anyway?

Loans longer than 30 years are typically non‑conforming and can’t be sold to Fannie Mae or Freddie Mac. That breaks the normal mortgage pipeline and adds cost and risk for lenders.

Will a 50‑year mortgage guarantee a much lower payment?

Not necessarily. Savings can be small—especially if longer terms carry higher rates. Several analyses call the reduction marginal.

What’s the biggest downside?

The lifetime interest cost. Over 50 years you could pay far more interest than with a 30‑year loan.

The Mortgage PTSD take — my practical advice

I understand why a longer term looks attractive when you’re squeezed. But based on what we know today:

- 50‑year mortgages are still a proposal, not a product you can get.

- There’s no timeline or rules yet.

- Even if they arrive, the tradeoff is likely large lifetime interest for a small monthly saving.

If you’re feeling pressure, don’t chase a product that doesn’t exist. Run real numbers on the options we have today: 30‑year fixed pricing, buydowns, purchase strategy adjustments, or modification paths in hardship. Clarity beats hype.

Final, honest point: No—50‑year mortgages aren’t available right now from qualified mortgage lenders in the U.S. But you still have options, and you don’t have to figure them out alone.